The Complete Buyer’s Guide | Yes Properties

How Much Deposit Do I Need to Buy a Property? (2026) | Complete Buyer’s Guide | Yes Properties

How Much Deposit Do I Need to Buy a Property?

Everything You Need to Know Before You Buy

Saving for a deposit is often the biggest hurdle for people looking to buy their first home. While many buyers focus on the purchase price, understanding how much deposit you need—and how it affects your mortgage—is just as important.

The amount you can put down as a deposit influences the size of your mortgage, the interest rates available and, ultimately, the overall cost of buying your home. Whether you’re a first-time buyer, moving home or investing in property, planning your deposit carefully can make a significant difference.

At Yes Properties, we help buyers understand every stage of the buying journey. This guide explains how deposits work, where they can come from and how to choose the approach that best suits your circumstances.

What Is a Property Deposit?

A property deposit is the portion of the purchase price that you pay using your own funds rather than borrowing from a mortgage lender.

For example:

If you’re buying a property for £400,000 and have a 10% deposit, you would contribute £40,000, while the remaining £360,000 would usually be funded through a mortgage, subject to lender approval.

The larger your deposit, the less you need to borrow.

Why Do Mortgage Lenders Require a Deposit?

A deposit reduces the lender’s risk.

By contributing your own money towards the purchase, you demonstrate financial commitment and reduce the amount the lender needs to finance.

Generally:

- Larger deposits reduce the lender’s exposure.

- Smaller mortgages may result in lower monthly repayments.

- Buyers with larger deposits often have access to a wider range of mortgage products.

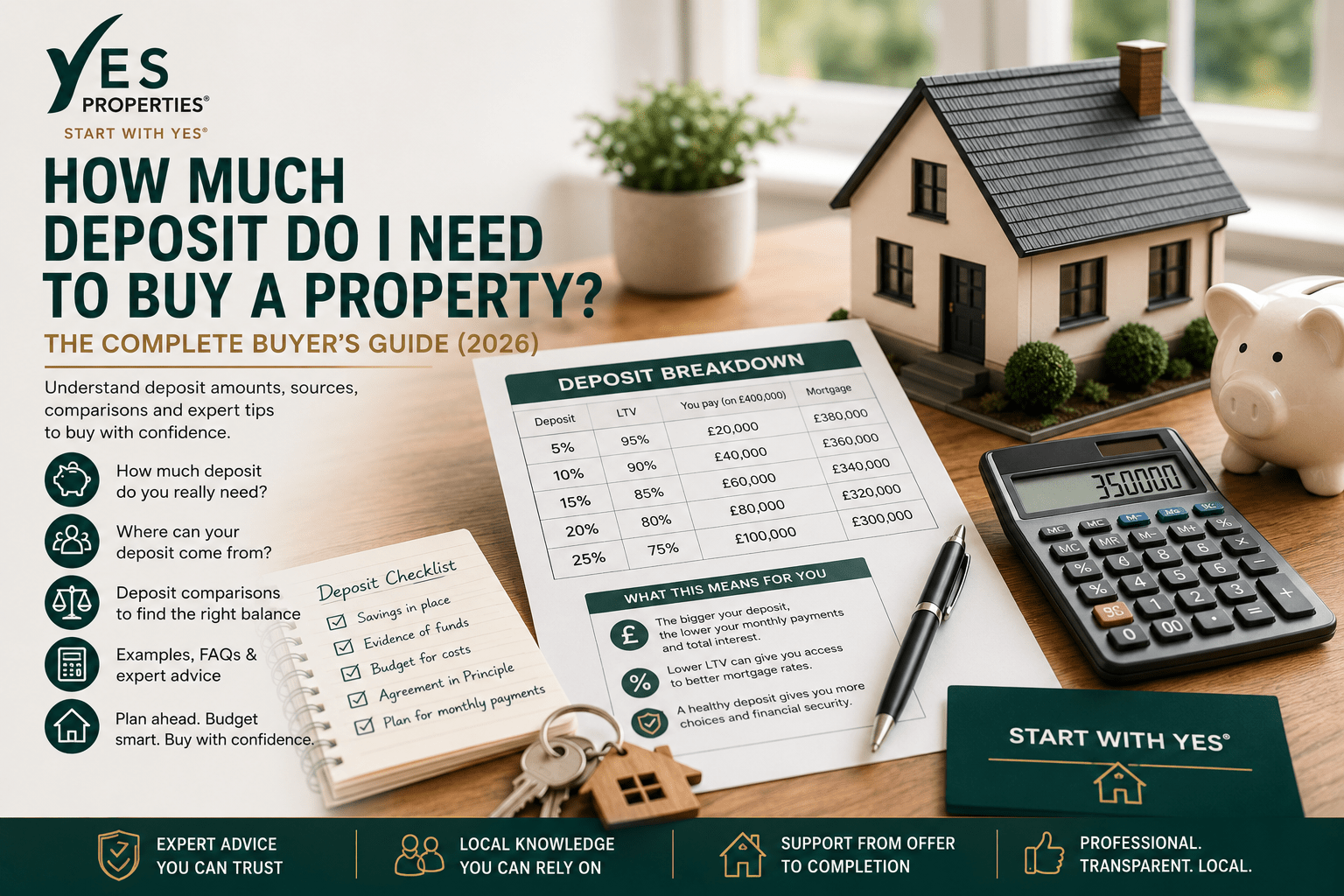

What Is Loan-to-Value (LTV)?

Loan-to-Value (LTV) is one of the most important mortgage terms you’ll encounter.

It represents the percentage of the property’s value that you are borrowing.

For example:

| Deposit | Mortgage | LTV |

|---|---|---|

| 5% | 95% | 95% |

| 10% | 90% | 90% |

| 15% | 85% | 85% |

| 20% | 80% | 80% |

| 25% | 75% | 75% |

As your deposit increases, your Loan-to-Value decreases.

A lower LTV is often viewed more favourably by lenders.

How Much Deposit Do You Need?

There is no single answer.

The amount depends on:

- Your finances.

- The property price.

- Your mortgage lender.

- Your mortgage product.

- Your affordability assessment.

Many buyers contribute somewhere between 5% and 25% of the purchase price, although individual circumstances vary.

Understanding Different Deposit Levels

5% Deposit

Often chosen by:

- First-time buyers.

- Buyers entering the property market sooner.

Advantages:

- Lower savings requirement.

- Earlier home ownership.

Things to consider:

- Higher Loan-to-Value.

- Fewer mortgage products may be available.

- Monthly repayments may be higher.

10% Deposit

A common target for many buyers.

Advantages include:

- Lower borrowing than a 5% deposit.

- Access to a wider choice of mortgage products.

- Potentially more competitive interest rates.

15% Deposit

Many lenders view an 85% LTV positively.

Potential benefits include:

- Greater product choice.

- Lower borrowing.

- Improved affordability.

20% Deposit

A substantial deposit can provide:

- Reduced monthly repayments.

- Lower overall borrowing.

- Access to more competitive mortgage rates.

25% Deposit and Above

Larger deposits may provide:

- Lower Loan-to-Value.

- Wider mortgage product choice.

- Greater financial flexibility.

However, buyers should also consider retaining sufficient savings for moving costs, furnishing and unexpected repairs.

YES Expert Tip: A larger deposit isn’t always the best solution if it leaves you with no financial buffer after completion. Aim for a balance between reducing borrowing and maintaining emergency savings.

Deposit Examples

| Property Price | 5% | 10% | 15% | 20% | 25% |

|---|---|---|---|---|---|

| £300,000 | £15,000 | £30,000 | £45,000 | £60,000 | £75,000 |

| £400,000 | £20,000 | £40,000 | £60,000 | £80,000 | £100,000 |

| £500,000 | £25,000 | £50,000 | £75,000 | £100,000 | £125,000 |

| £600,000 | £30,000 | £60,000 | £90,000 | £120,000 | £150,000 |

| £700,000 | £35,000 | £70,000 | £105,000 | £140,000 | £175,000 |

Does a Bigger Deposit Always Mean a Better Mortgage?

Not necessarily.

While a larger deposit can improve your options, lenders also consider:

- Income.

- Affordability.

- Employment.

- Credit history.

- Existing financial commitments.

A larger deposit is only one part of the overall mortgage assessment.

YES Expert Tip: Before deciding how much to put down as a deposit, speak to a qualified mortgage adviser or broker. They can help you understand how different deposit levels may affect your borrowing options and overall affordability.

How Much Deposit Do I Need to Buy a Property? (2026)

Part 2 – Where Can Your Property Deposit Come From?

Once you’ve decided how much deposit you’d like to put down, the next question is where that money can come from.

Mortgage lenders and conveyancing solicitors don’t just need to know how much your deposit is—they also need to understand where it has come from. This is an important part of the home-buying process and helps protect against fraud and financial crime.

Whether you’ve spent years saving, received financial support from family or are using proceeds from another property sale, it’s important to understand what evidence may be required before your purchase can proceed.

Personal Savings

The most common source of a property deposit is personal savings.

These may include:

- Savings accounts

- Cash ISAs

- Fixed-term savings

- Premium Bonds (once redeemed)

- Regular savings accounts

- Investment accounts (after funds have been realised)

Your solicitor will usually ask for bank statements showing how the funds have accumulated and where they are currently held.

Lifetime ISA (LISA)

A Lifetime ISA (LISA) is a government-backed savings product designed to help eligible individuals save towards their first home or retirement.

Eligible savers can benefit from a government bonus on qualifying contributions, subject to the scheme rules in force at the time.

If you’re planning to use a Lifetime ISA:

- Tell your conveyancing solicitor early.

- Allow sufficient time for the funds to be released.

- Ensure the purchase meets the scheme requirements.

YES Expert Tip: Don’t wait until the last minute to mention your Lifetime ISA. Releasing funds can take time, so letting your solicitor know early can help avoid delays.

Gifted Deposits

Many first-time buyers receive financial assistance from family members.

This is commonly known as a gifted deposit.

A gifted deposit is money that is genuinely given to you and does not need to be repaid.

Mortgage lenders and solicitors will usually require confirmation that:

- The money is a genuine gift.

- The donor will not acquire an ownership interest in the property (unless otherwise agreed).

- The donor understands the nature of the gift.

Supporting documentation is commonly required.

Family Assistance

Parents, grandparents and other close relatives often help buyers onto the property ladder.

Support may include:

- Cash gifts.

- Early inheritance.

- Savings contributions.

- Assistance with moving costs.

Every lender has its own requirements, so it’s important to discuss family contributions with your mortgage adviser before making an application.

Inheritance

Some buyers use money received through an inheritance to fund all or part of their deposit.

Solicitors may ask for documentation confirming the origin of the funds, particularly where large sums are involved.

Sale of Another Property

Home movers often use the equity from the sale of their existing property as the deposit for their next purchase.

Your conveyancer will usually coordinate both transactions to ensure the sale proceeds are available in time for completion.

Investment Proceeds

Some buyers use money realised from investments such as:

- Shares

- Investment funds

- Bonds

- Unit trusts

If this applies to you, your solicitor may request evidence showing how the funds were generated and transferred.

Overseas Funds

Using money held overseas is often possible, but additional checks may be required.

These can include:

- Source of funds evidence.

- Certified identification documents.

- Currency conversion records.

- Bank statements.

- Translation of documents where necessary.

If you intend to use overseas funds, inform both your mortgage adviser and conveyancer as early as possible.

Source of Funds Checks

One of the most important parts of the buying process is verifying the Source of Funds.

Your solicitor must be satisfied that the money being used for the purchase comes from legitimate sources.

Depending on your circumstances, you may be asked to provide:

- Bank statements.

- Savings history.

- Investment statements.

- Property sale statements.

- Probate documents.

- Gifted deposit declarations.

- Evidence of bonuses or inheritance.

These checks are a legal requirement and form part of the conveyancing process.

Anti-Money Laundering (AML) Checks

Solicitors and estate agents are legally required to comply with Anti-Money Laundering (AML) regulations.

These checks are designed to help prevent:

- Fraud.

- Money laundering.

- Terrorist financing.

- Financial crime.

As part of these obligations, you may be asked to provide:

- Proof of identity.

- Proof of address.

- Evidence of the source of your funds.

- Information about the source of your wealth (where appropriate).

While the process can feel detailed, it helps protect both buyers and the wider property market.

Joint Buyers

If you’re buying jointly, each buyer’s contribution may need to be verified separately.

Your solicitor may ask for:

- Individual bank statements.

- Identification documents.

- Source of funds evidence.

- Details of each person’s financial contribution.

Being organised from the outset can help keep the transaction moving smoothly.

Self-Employed Buyers

If you’re self-employed, using your own savings for a deposit is no different in principle from any other buyer.

However, lenders may also wish to assess your financial position through documents such as:

- Tax calculations (SA302s).

- Tax Year Overviews.

- Business accounts.

- Accountant’s confirmation.

- Business and personal bank statements.

Providing accurate information at an early stage can help avoid unnecessary delays.

What You Cannot Normally Use

Certain sources of money may raise concerns with lenders or solicitors.

For example, additional enquiries may be required if the deposit comes from:

- Unexplained cash deposits.

- Undocumented loans.

- Unknown third parties.

- Funds that cannot be evidenced.

- Complex financial arrangements without supporting documentation.

Always discuss your circumstances openly with your mortgage adviser and conveyancer so they can advise on the appropriate evidence required.

Deposit Comparison: Personal Savings vs Gifted Deposit

| Personal Savings | Gifted Deposit |

|---|---|

| Built up over time | Provided by someone else |

| No donor paperwork | Gift declaration usually required |

| Straightforward evidence | Additional lender and solicitor checks |

| Full control over funds | Donor may need to provide identification and evidence of funds |

Neither option is inherently better—the key is ensuring the source of the funds can be clearly evidenced.

Deposit Comparison: Lifetime ISA vs Standard Savings

| Lifetime ISA | Standard Savings |

|---|---|

| Government bonus available (subject to scheme rules) | No government bonus |

| Eligibility conditions apply | Greater flexibility |

| Designed for qualifying first-home purchases or retirement | Can generally be used for any purpose |

| Withdrawal rules apply | Immediate access depends on account type |

Common Mistakes Buyers Make

Avoid these common pitfalls:

❌ Transferring money between multiple accounts without keeping records.

❌ Waiting until the last minute to tell your solicitor about a gifted deposit.

❌ Assuming overseas funds require no additional checks.

❌ Failing to retain evidence of savings.

❌ Believing AML checks are optional.

❌ Trying to hide the true source of funds.

YES Expert Tip: Keep a clear paper trail for your deposit. Whether the money comes from savings, a gift or the sale of another property, organised records can help your solicitor complete the required checks more efficiently.

How Much Deposit Do I Need to Buy a Property? (2026)

Part 3 – Comparing Different Deposit Strategies

There is no single “perfect” deposit size. The right amount depends on your financial circumstances, long-term goals and how quickly you want to buy.

Some buyers prefer to purchase as soon as possible with a smaller deposit, while others choose to save for longer in order to reduce their borrowing and access a wider choice of mortgage products.

This section compares the most common deposit strategies to help you decide which approach best suits your circumstances.

5% Deposit vs 10% Deposit

This is one of the most common decisions facing first-time buyers.

| 5% Deposit | 10% Deposit |

|---|---|

| Smaller amount to save | Larger upfront savings required |

| Buy sooner | May take longer to save |

| Higher Loan-to-Value (95%) | Lower Loan-to-Value (90%) |

| Mortgage payments may be higher | Borrow less overall |

| Fewer mortgage products may be available | Often wider mortgage choice |

Which Is Better?

A 5% deposit can help buyers enter the market sooner, while a 10% deposit may provide greater flexibility and potentially more competitive mortgage products.

There is no universal answer—it depends on your financial position and personal goals.

10% Deposit vs 20% Deposit

Many buyers wonder whether it’s worth waiting to save a much larger deposit.

| 10% Deposit | 20% Deposit |

|---|---|

| Buy earlier | Save for longer |

| Larger mortgage | Smaller mortgage |

| Higher monthly repayments | Lower monthly repayments |

| More interest paid over time | Less interest over the mortgage term |

| Good product choice | Often access to more competitive products |

Waiting longer may reduce borrowing, but delaying a purchase could also mean missing opportunities if property prices rise.

Small Deposit vs Large Deposit

Small Deposit

Advantages:

- Buy sooner.

- Enter the property market earlier.

- Potentially benefit from future property price growth.

Considerations:

- Higher borrowing.

- Higher monthly repayments.

- Higher Loan-to-Value.

Large Deposit

Advantages:

- Smaller mortgage.

- Lower monthly repayments.

- Greater financial flexibility.

- Lower overall borrowing.

Considerations:

- Longer saving period.

- Possible delay in purchasing.

- Opportunity cost if property prices increase while saving.

YES Expert Tip: Don’t focus solely on achieving the largest possible deposit. Buying a suitable home at the right time may be more beneficial than waiting years to save a larger amount.

Buying Sooner vs Saving Longer

This is another question many buyers ask.

Buying Sooner

Potential advantages:

- Begin building equity earlier.

- Stop paying rent sooner (where applicable).

- Benefit from any future property price growth.

Potential considerations:

- Higher mortgage.

- Smaller financial buffer.

- Fewer mortgage options.

Saving Longer

Potential advantages:

- Larger deposit.

- Reduced borrowing.

- Lower monthly repayments.

- Greater choice of mortgage products.

Potential considerations:

- Delayed purchase.

- Property prices may change while saving.

- Interest rates may also change.

There is no universally correct answer. The right decision depends on your finances, housing needs and long-term plans.

Personal Savings vs Gifted Deposit

Many buyers rely on family support to purchase their first home.

Personal Savings

Advantages:

- Complete financial independence.

- Straightforward evidence of funds.

- No reliance on third parties.

Gifted Deposit

Advantages:

- Buy sooner.

- Larger deposit.

- Reduced borrowing.

Additional considerations:

- Gift declarations are usually required.

- Lenders and solicitors will normally carry out additional checks.

- The donor may need to provide identification and evidence of the source of the gifted funds.

Lifetime ISA vs Standard Savings

For eligible first-time buyers, a Lifetime ISA can provide valuable government support.

Lifetime ISA

Advantages:

- Government bonus on qualifying contributions.

- Specifically designed to help eligible first-time buyers and retirement savers.

- Can help build a deposit more quickly.

Considerations:

- Eligibility criteria apply.

- Property price limits and other scheme rules must be met.

- Withdrawal conditions apply.

Standard Savings

Advantages:

- Greater flexibility.

- No scheme restrictions.

- Can be used for any property purchase.

Considerations:

- No government bonus.

Single Buyer vs Joint Buyer

Buying with another person can increase affordability, but it also involves shared financial responsibility.

Buying Alone

Advantages:

- Full ownership.

- Independent financial decisions.

- No need to coordinate finances with another buyer.

Considerations:

- Single income assessment.

- Smaller borrowing capacity in some cases.

Buying Jointly

Advantages:

- Combined income.

- Larger borrowing potential.

- Shared deposit.

- Shared monthly mortgage payments.

Considerations:

- Joint responsibility for the mortgage.

- Both buyers’ financial circumstances are assessed.

- Decisions regarding ownership and future sale should be discussed carefully.

Cash Buyer vs Mortgage Buyer

Although most buyers require a mortgage, some purchase using cash.

Cash Buyer

Advantages:

- No mortgage required.

- Faster transactions in many cases.

- No mortgage valuation.

- No mortgage lender conditions.

Considerations:

- Large amount of capital tied up in the property.

- Opportunity cost of using cash rather than other investments.

Mortgage Buyer

Advantages:

- Requires less upfront capital.

- Allows buyers to spread the purchase cost over time.

- Enables many people to purchase sooner.

Considerations:

- Interest payable.

- Mortgage affordability assessments.

- Lender requirements.

- Ongoing monthly repayments.

Real-Life Deposit Examples

Example 1 – First-Time Buyer

- Property Price: £350,000

- Deposit: 5% (£17,500)

- Mortgage Required: £332,500

This allows earlier entry to the market but involves a higher Loan-to-Value.

Example 2 – Growing Family

- Property Price: £600,000

- Deposit: 20% (£120,000)

- Mortgage Required: £480,000

A larger deposit reduces borrowing and may provide access to more competitive mortgage products.

Example 3 – Downsizer

A homeowner selling an existing property may use equity from the sale to provide a substantial deposit, reducing the amount they need to borrow for their next home.

Example 4 – First-Time Buyer with Family Support

A buyer uses:

- Personal savings.

- A Lifetime ISA.

- A gifted deposit from parents.

This combination can significantly strengthen the overall deposit, provided the lender’s and solicitor’s requirements are met.

Which Deposit Strategy Is Right for You?

Ask yourself:

- How quickly do I want to buy?

- How much can I comfortably save?

- Do I have an emergency fund?

- Will I still have savings after completion?

- Am I receiving family assistance?

- What are current mortgage rates?

- Am I comfortable with the proposed monthly repayments?

These questions can help you determine the most suitable deposit strategy for your individual circumstances.

Common Mistakes Buyers Make

Avoid these common pitfalls:

❌ Waiting indefinitely for the “perfect” deposit.

❌ Spending every available penny on the deposit.

❌ Ignoring the total cost of buying.

❌ Assuming a larger deposit always guarantees the best mortgage.

❌ Failing to budget for unexpected expenses after moving.

❌ Forgetting to maintain an emergency savings fund.

YES Expert Tip: The best deposit isn’t necessarily the biggest one—it’s the one that allows you to buy a suitable property while keeping your finances healthy and sustainable.

How Much Deposit Do I Need to Buy a Property? (2026)

Part 4 – Frequently Asked Questions, Deposit Myths & Common Mistakes

By now, you should have a good understanding of how property deposits work and where they can come from. However, there are still several questions that buyers regularly ask before making an offer.

This section answers some of the most common questions and dispels a number of myths surrounding property deposits in England.

Can I Buy a Property With No Deposit?

In most cases, buyers will need to contribute a deposit towards the purchase.

While some mortgage products may allow buyers to borrow a very high percentage of a property’s value, eligibility depends on the lender’s criteria and the products available at the time.

If you have little or no deposit, it may be worth discussing your options with a qualified mortgage adviser or broker, who can explain what products may be suitable for your circumstances.

Can I Borrow My Deposit?

Mortgage lenders generally expect your deposit to come from your own funds or an acceptable source, such as savings or a genuine gift.

If you intend to use borrowed money as your deposit, you should tell your lender and mortgage adviser. Borrowing additional money may affect affordability and the lender’s decision.

Failing to disclose relevant financial commitments could cause delays or complications with your application.

Can My Parents Give Me My Deposit?

Yes, many buyers receive financial assistance from parents or other close family members.

This is commonly known as a gifted deposit.

Lenders and solicitors will usually require:

- A gifted deposit declaration.

- Confirmation that the money is a genuine gift.

- Proof of identity for the donor.

- Evidence of the source of the gifted funds.

Each lender has its own requirements, so it’s sensible to discuss this with your mortgage adviser before applying.

Can I Use Cryptocurrency?

If your deposit is derived from cryptocurrency investments, your solicitor and lender may require additional evidence showing:

- Ownership of the assets.

- Sale of the cryptocurrency.

- Transfer of funds into your bank account.

- Source of the original investment.

Because cryptocurrency transactions can involve additional compliance checks, it’s advisable to discuss this with your conveyancer at an early stage.

Can I Use Overseas Money?

Yes, many buyers use funds held overseas.

However, additional documentation may be required, including:

- Overseas bank statements.

- Currency conversion records.

- Certified translations where appropriate.

- Source of funds evidence.

- Identity verification.

International transfers can take time, so informing your solicitor early can help prevent delays.

What Happens if the Property Is Valued for Less Than the Agreed Price?

Sometimes the lender’s valuation is lower than the price you’ve agreed to pay.

This is often referred to as a down valuation.

Possible outcomes include:

- Renegotiating the purchase price with the seller.

- Increasing your deposit.

- Choosing another lender (where appropriate).

- Deciding not to proceed with the purchase.

Your mortgage adviser and conveyancer can explain the options available based on your individual circumstances.

Does My Deposit Affect My Mortgage Interest Rate?

In many cases, yes.

A larger deposit generally results in a lower Loan-to-Value (LTV) ratio, which may provide access to a wider choice of mortgage products and, in some cases, more competitive interest rates.

However, interest rates also depend on other factors, including your financial circumstances and the lender’s lending criteria.

Should I Use All My Savings as a Deposit?

Not necessarily.

Although increasing your deposit may reduce the amount you need to borrow, it’s usually sensible to retain some savings for:

- Legal fees.

- Surveys.

- Moving costs.

- Furniture.

- Decorating.

- Emergency repairs.

- Unexpected household expenses.

A financial safety net can provide valuable peace of mind after you move into your new home.

YES Expert Tip: Buying a home is only the beginning. Keeping an emergency fund can help you deal with unexpected repairs without putting unnecessary pressure on your finances.

Common Deposit Myths

“I Need a 20% Deposit to Buy a House.”

Myth.

Some buyers purchase with smaller deposits, subject to lender criteria and the availability of suitable mortgage products.

“The Bigger My Deposit, the Better.”

Not always.

While a larger deposit may reduce borrowing, it should not leave you without sufficient savings for the costs of buying and maintaining your home.

“Gifted Deposits Are Not Allowed.”

Incorrect.

Many lenders accept gifted deposits, provided the appropriate documentation and checks are completed.

“The Deposit Is the Only Money I Need.”

False.

You should also budget for:

- Solicitor’s fees.

- Surveys.

- Stamp Duty (where applicable).

- Insurance.

- Removal costs.

- Initial home improvements.

“My Mortgage Will Definitely Be Approved Because I Have a Large Deposit.”

Not necessarily.

Lenders also assess:

- Income.

- Employment.

- Affordability.

- Credit history.

- Existing financial commitments.

A larger deposit is only one part of the mortgage assessment.

Buyer’s Deposit Checklist

Before making an offer, make sure you can answer YES to the following:

✓ I know how much deposit I have available.

✓ I understand where my deposit is coming from.

✓ I can provide evidence of my funds if required.

✓ I have considered solicitor’s fees and other buying costs.

✓ I have arranged or intend to arrange an Agreement in Principle.

✓ I understand my likely monthly mortgage repayments.

✓ I have retained some emergency savings.

✓ I understand the total cost of buying, not just the deposit.

Common Mistakes Buyers Make

Avoid these common pitfalls:

❌ Waiting too long to begin saving.

❌ Moving money between multiple accounts without retaining evidence.

❌ Forgetting about additional buying costs.

❌ Assuming a gifted deposit requires no paperwork.

❌ Using all available savings as the deposit.

❌ Not discussing unusual sources of funds with your solicitor at an early stage.

❌ Believing that a larger deposit guarantees mortgage approval.

YES Expert Tip: Being organised is just as important as saving the money itself. Keeping clear records and speaking to professionals early can make the buying process much smoother.

Why Choose Yes Properties?

At Yes Properties, we understand that saving for a deposit can feel like one of the biggest challenges when buying a home. That’s why we aim to provide clear, practical guidance to help buyers understand not only how much deposit they need, but also the wider financial considerations involved in purchasing a property.

Whether you’re buying your first home, moving up the property ladder or investing in residential property, our experienced team is here to guide you through every stage of the process.

We offer:

- Honest and straightforward advice.

- Local market expertise.

- Guidance throughout the buying process.

- Professional negotiation.

- Sales progression support.

- Regular communication from offer to completion.

START WITH YES®

Looking to buy your next home?

Yes Properties

15 Morden Court Parade

London Road

Morden

SM4 5HJ

📞 Telephone: 0208 191 3717

✉️ Email: info@yesproperties.co.uk

Professional. Transparent. Local.

START WITH YES®

Related Guides

Continue your buying journey with:

- Complete First-Time Buyer’s Guide

- Buying Leasehold Property

- Buying Freehold Property

- Mortgage Agreement in Principle Explained

- Property Surveys Explained

- Hidden Costs of Buying Property

- Stamp Duty Guide

- What Is Exchange of Contracts?

- Completion Day Explained

- Buying a Probate Property

Conclusion

Saving for a property deposit is one of the most significant milestones in the home-buying journey. While the size of your deposit plays an important role in determining how much you can borrow and the mortgage products available to you, it’s equally important to understand where your funds come from, keep clear records and budget for the many other costs involved in buying a home.

By planning ahead, maintaining an emergency fund and seeking professional advice when needed, you’ll be in a much stronger position to purchase your new home with confidence.

At Yes Properties, we’re committed to helping buyers make informed decisions at every stage of the buying process—providing trusted local expertise, practical guidance and professional support from your first enquiry through to completion.

START WITH YES®

How Much Deposit Do I Need to Buy a Property? (2026)

Part 5 – Deposit Calculator, Real-Life Examples & Final Buyer’s Guide

Understanding percentages is one thing—but seeing real examples can make planning your property purchase much easier.

This final section provides practical deposit examples, explains how different deposit sizes affect your mortgage, and includes a handy checklist to help you prepare before making an offer.

Property Deposit Calculator

The table below shows how much you’ll need to save for some common purchase prices.

| Property Price | 5% Deposit | 10% Deposit | 15% Deposit | 20% Deposit | 25% Deposit |

|---|---|---|---|---|---|

| £200,000 | £10,000 | £20,000 | £30,000 | £40,000 | £50,000 |

| £250,000 | £12,500 | £25,000 | £37,500 | £50,000 | £62,500 |

| £300,000 | £15,000 | £30,000 | £45,000 | £60,000 | £75,000 |

| £350,000 | £17,500 | £35,000 | £52,500 | £70,000 | £87,500 |

| £400,000 | £20,000 | £40,000 | £60,000 | £80,000 | £100,000 |

| £450,000 | £22,500 | £45,000 | £67,500 | £90,000 | £112,500 |

| £500,000 | £25,000 | £50,000 | £75,000 | £100,000 | £125,000 |

| £600,000 | £30,000 | £60,000 | £90,000 | £120,000 | £150,000 |

| £700,000 | £35,000 | £70,000 | £105,000 | £140,000 | £175,000 |

| £800,000 | £40,000 | £80,000 | £120,000 | £160,000 | £200,000 |

| £900,000 | £45,000 | £90,000 | £135,000 | £180,000 | £225,000 |

| £1,000,000 | £50,000 | £100,000 | £150,000 | £200,000 | £250,000 |

YES Expert Tip: Remember that your deposit is only one part of your overall budget. You’ll also need to allow for solicitor’s fees, surveys, Stamp Duty (where applicable), removal costs and other buying expenses.

Real-Life Buying Scenarios

Scenario 1 – First-Time Buyer

Purchase Price: £325,000

- Deposit: £16,250 (5%)

- Mortgage: £308,750

Ideal for buyers who want to get onto the property ladder sooner, provided they are comfortable with a higher Loan-to-Value mortgage.

Scenario 2 – Couple Buying Their First Family Home

Purchase Price: £550,000

- Deposit: £55,000 (10%)

- Mortgage: £495,000

A 10% deposit is a common target and may provide access to a wider range of mortgage products than a 5% deposit.

Scenario 3 – Home Mover

A homeowner sells their existing property and uses part of the equity as a 20% deposit on their next purchase.

Benefits may include:

- Lower Loan-to-Value.

- Reduced borrowing.

- Lower monthly repayments.

- Greater choice of mortgage products.

Scenario 4 – First-Time Buyer with Family Support

Purchase Price: £450,000

Deposit made up of:

- Personal savings

- Lifetime ISA savings

- Gifted deposit from parents

Provided all lender and solicitor requirements are satisfied, this can strengthen the buyer’s overall financial position.

Scenario 5 – Property Investor

An investor purchasing a buy-to-let property may choose to contribute a larger deposit to reduce borrowing and improve cash flow.

Mortgage products for investment properties often differ from those available for owner-occupiers, so specialist advice is recommended.

How to Save for a Deposit

Saving for a deposit takes time and discipline.

Many buyers find the following strategies helpful:

- Set a monthly savings target.

- Open a dedicated savings account.

- Automate regular transfers.

- Reduce unnecessary spending.

- Pay off expensive debt where possible.

- Save bonuses separately.

- Avoid dipping into your deposit fund.

- Review your progress regularly.

Even small, consistent contributions can make a significant difference over time.

Deposit Planning Timeline

12–24 Months Before Buying

- Start saving regularly.

- Review your credit report.

- Reduce unnecessary debt.

- Consider opening a Lifetime ISA if eligible.

6–12 Months Before Buying

- Research local property prices.

- Estimate your budget.

- Gather proof of savings.

- Speak to a mortgage adviser if appropriate.

1–3 Months Before Buying

- Obtain an Agreement in Principle.

- Choose a conveyancing solicitor.

- Organise proof of identity and source of funds.

- Begin viewing suitable properties.

After Your Offer Is Accepted

- Submit your full mortgage application.

- Arrange your survey.

- Respond promptly to requests from your solicitor and lender.

- Prepare your deposit funds for completion.

Deposit Planning Checklist

Before making an offer, make sure you can answer YES to the following:

✔ I understand how much deposit I have.

✔ I know where my deposit is coming from.

✔ I have evidence of my savings or gifted funds.

✔ I have obtained (or plan to obtain) an Agreement in Principle.

✔ I have budgeted for solicitor’s fees.

✔ I have allowed for survey costs.

✔ I understand any Stamp Duty liability.

✔ I have an emergency fund.

✔ I have budgeted for moving costs.

✔ I know my likely monthly mortgage repayments.

Frequently Asked Questions

Is a larger deposit always better?

Not necessarily. A larger deposit can reduce borrowing and may improve your mortgage options, but it’s usually sensible to retain enough savings for moving costs, repairs and unexpected expenses.

Can I increase my deposit after receiving an Agreement in Principle?

Potentially, yes. However, you’ll need to discuss any changes with your mortgage adviser or lender, as they may affect your mortgage application.

Should I wait until I’ve saved a 20% deposit?

There is no universal answer. Some buyers prefer to purchase sooner with a smaller deposit, while others choose to wait and save more. The right approach depends on your financial circumstances, housing needs and long-term goals.

Will a gifted deposit affect my mortgage?

Many lenders accept gifted deposits, but they will usually require additional documentation to confirm the source of the funds and that the money is a genuine gift.

Can I use money from the sale of another property?

Yes. Home movers commonly use equity released from the sale of their existing property as the deposit for their next purchase.

Common Mistakes Buyers Make

Avoid these common pitfalls:

❌ Focusing only on saving the deposit.

❌ Forgetting about legal fees and surveys.

❌ Spending all available savings on the purchase.

❌ Not keeping evidence of the source of funds.

❌ Delaying conversations with mortgage advisers or solicitors.

❌ Ignoring the impact of monthly mortgage repayments on everyday living costs.

YES Expert Tip: Buying a home should strengthen your financial future—not put it under unnecessary pressure. A realistic budget that includes both the purchase and the ongoing costs of homeownership will help you enjoy your new property with confidence.

Why Choose Yes Properties?

At Yes Properties, we know that buying a home is about much more than simply finding the right property. It’s about making informed financial decisions and understanding every stage of the buying journey.

Our experienced team provides:

- Honest, straightforward advice.

- Local market knowledge.

- Guidance throughout the buying process.

- Professional negotiation.

- Sales progression support.

- Clear communication from offer to completion.

Whether you’re a first-time buyer, moving home or investing in property, we’re here to help you every step of the way.

START WITH YES®

Ready to take the next step?

Yes Properties

15 Morden Court Parade

London Road

Morden

SM4 5HJ

📞 Telephone: 0208 191 3717

✉️ Email: info@yesproperties.co.uk

Professional. Transparent. Local.

START WITH YES®

Related Guides

Continue your buying journey with:

- Complete First-Time Buyer’s Guide

- Buying Leasehold Property

- Buying Freehold Property

- Mortgage Agreement in Principle Explained

- Property Surveys Explained

- Hidden Costs of Buying Property

- Stamp Duty Guide

- What Is Exchange of Contracts?

- Completion Day Explained

- Buying a Probate Property

Conclusion

Your deposit is one of the most important parts of buying a property, but it’s only one piece of the puzzle. Understanding how much you need, where your funds can come from, and how your deposit affects your mortgage will help you make confident and informed decisions.

By planning early, keeping clear records and maintaining a realistic budget, you’ll be in a stronger position to secure the right property while protecting your financial wellbeing.

At Yes Properties, we’re committed to helping buyers navigate every stage of the home-buying process with trusted advice, local expertise and professional support.

START WITH YES®